Cultivator

Get in-built smarts to do the work

Plum Retirement Income - Cultivator

Cultivator is like a plant that looks after itself. It’s an automated investment and drawdown strategy, designed to deliver income stability over the short to medium term and growth over the long-term so your money lasts as long as possible.

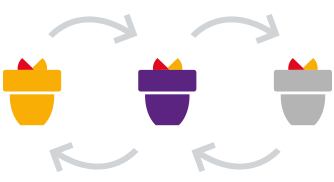

With its inbuilt smarts, Cultivator invests your account balance across three investment pots and reviews and (where appropriate) rebalances investments quarterly using automated asset allocation strategies that aim to optimise retirement incomes. The automated approach reduces the tendency for investors to react to every market move, which can help protect your retirement savings.

How your money is allocated in Cultivator

Your money is divided across the three investment pots, depending on your annual income requirements.

MLC Cash (Pension)

This pot aims to maintain three years' worth of your nominated annual pension payment amount, with a little bit set aside to cover your fees. It does this by investing in cash assets.

MLC Conservative Balanced (Pension)

This pot aims to maintain investment value, up to six years worth of your nominated annual pension payment amount. It does this with a balanced mixed of defensive and growth assets.

MLC Growth (Pension)

This pot aims to achieve long term growth, through a higher investment allocation to growth assets than the other pots. While its returns may fluctuate more over the short term, it's expected to produce higher returns over the long term.

How assets are allocated

Depending on your annual income requirements when starting your pension, your money is divided into three investment options.

Example: John, 60 years of age

John is 60 years of age and starts his pension with a balance of $500,000. He chooses to receive 5% of his account balance as income each year, which is taken from his short-term pot.

This is how his balance will be invested:

MLC Cash

(Pension)

3 x annual income

1 Year = $500,000 x 5% ($25,000)

= 3 x $25,000

= $75,000

MLC Conservative

Balanced (Pension)

6 x annual income

$500,000 x 5% ($25,000)

= 6 x $25,000

= $150,000

MLC Growth

(Pension)

Remainder

$500,000 - $75,000 - $150,000

= $275,000

*The examples above are for illustrative purposes only and are not an estimate or guarantee of your account balance, the pension payments that will be made to you or the actual allocations that will be applied in respect to your account. The actual allocation may differ due to regular provisioning of fee deductions from MLC Cash (Pension). John is not an actual Plum Super member.

Get growing

The account based pension in Plum Retirement Income is based on the amount you choose to invest in your account. It’s not a guaranteed income for life, so it’s important to determine whether it’s right for you.

To open a Plum Retirement Income account log onto your online account, call us at 1300 55 7586 from Monday to Friday between 8am to 7pm (AEST) or chat with us online.

Things to consider

NULIS Nominees (Australia) Limited is the trustee of the MLC Super Fund ABN 70 732 426 024 and the issuer of Plum Retirement Income product. Plum is a division of the MLC Super Fund. A Product Disclosure Statement (PDS) for the Plum Retirement Income Product is available at plum.com.au/PRI or by calling 1300 55 7586. You should obtain and consider the PDS for this product before making any decision about whether to acquire or continue to hold the product. Any advice or information provided is general only, and has been prepared without taking into account your particular circumstances and needs. Before acting on any advice on this website you should assess or seek advice on whether it is appropriate for your needs, financial situation and investment objectives. Any general tax information provided in this publication is intended as a guide only and is based on our general understanding of taxation laws. It is not intended to be a substitute for specialised taxation advice or an assessment of your liabilities, obligations or claim entitlements that arise, or could arise, under taxation law, and we recommend you consult with a registered tax agent. You should also remember that past performance is not a reliable indicator of future performance. The information in this document is current as at 29 September 2023. It may be subject to change into the future © NULIS Nominees (Australia) 2017.

Any phone based general advice or application service provided for the Plum Retirement Income product is provided by Actuate Alliance Services Pty Ltd ABN 40 083 233 925, AFSL 240959. Actuate Alliance Services Pty Ltd and NULIS Nominees (Australia) Limited ABN 80 008 515 633 AFSL 236465 are part of the Insignia Financial Group of Companies. An investment with NULIS Nominees (Australia) Limited is not a deposit or liability of, and is not guaranteed by Insignia Financial Ltd ABN 49 100 103 722 and its related bodies corporate (Insignia Financial Group). Insignia Financial does not guarantee or otherwise accept any liability in respect of this product.

Call us on 1300 55 7586

Call us on 1300 55 7586

Outside of Australia call +61 3 7073 3050

Monday to Friday between 8am to 7pm (AEST)

Download the PDS

Download the PDS

Review the Plum Retirement Income PDS for more information.