Will the Iran War generate a global energy & food crisis?

April 2026

Bob Cunneen, Senior Economist and Portfolio Specialist

6 min read

“The war in the Middle East is creating the largest supply disruption in the history of the global oil market. With crude and oil product flows through the Strait of Hormuz plunging from around 20 million barrels per day before the war to a trickle currently...” 1

International Energy Agency (IEA), March 2026

“Living in the 1970s”

The Middle East is engulfed in a war that is destroying lives. The attack on 28 February 2026 by the US and Israel on Iran has also ignited a wide array of economic consequences that could prove devastating. Iran has responded to this sudden attack by effectively closing the Strait of Hormuz. The Strait of Hormuz is a key maritime transport corridor for the commodity exports of the Gulf States which includes Saudi Arabia, Iraq, United Arab Emirates (UAE), Kuwait as well as Iran. Given this sudden commodity supply shortage, sharp price rises have been recorded in oil, natural gas and fertiliser.

The economic impact of the Iran War could prove to be as dramatic as the ‘1970s Oil Shocks’. The global economy currently confronts the prospect of both rising inflation and unemployment because of this Iran War. This ‘stagflation’ mix of both higher inflation and unemployment creates a major policy dilemma for central banks. Should central banks raise interest rates to restrain inflation pressures or lower interest rates to support economic activity and mitigate rising unemployment?

Oil prices can make your blood boil

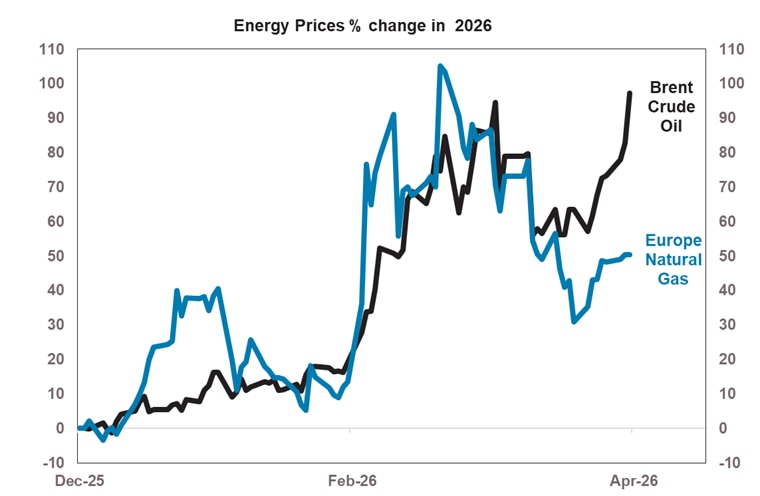

Global crude oil prices have surged by 97% in US dollar terms this year given the sudden shutdown of the Strait of Hormuz (Chart 1). While the impact on Australian motorists has been partly mitigated by a rising Australian dollar and the Federal Government’s decision to cut fuel excise taxes by twenty-six cents until June, the shock is still there for household budgets.

Chart 1: Global crude oil prices have surged this year

Source: LSEG Datastream. Brent oil price is Crude Oil BFO M1 Europe FOB $/BBl. Natural gas is LNG Natural Gas. Data as at 30/04/2026.

Another symptom of this global energy crisis is soaring natural gas prices. Approximately 20% of the global supply of Liquid Natural Gas (LNG) is sourced from Qatar and the UAE. Given the damage sustained to Qatar’s and UAE’s gas production facilities by Iran’s attack as well as the inability to transport LNG, there has been a +50% surge in natural gas prices this year. These rising energy costs have widespread dramatic implications for the global price of goods. The cost of producing plastic packaging, PVC pipes and even garbage bags is heading higher given plastic’s dependence on cheap energy.

Is a global food crisis looming?

“The 2026 conflict in the Middle East is adding further pressure on fragile agrifood systems and global supply chains, threatening the availability, accessibility, and affordability of food”.2

Food and Agriculture Organization of the United Nations (FAO)

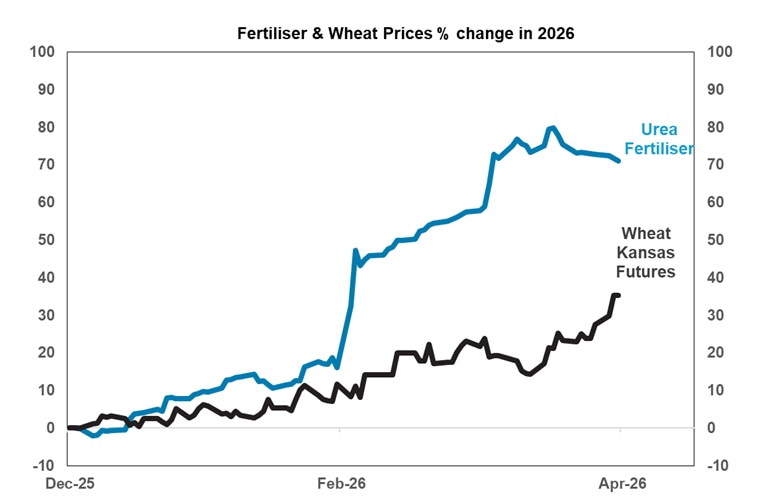

As the FAO has highlighted in recent research, the Iran War is a threat to food prices. The Strait of Hormuz carries approximately 20% of the global trade in fertilisers. Given their access to cheap energy, Gulf countries such as Qatar and Saudi Arabia are key suppliers of nitrogen fertilisers, such as Urea and Ammonia, as well as Sulphur, which is a major input into producing phosphate fertilisers. The Urea fertiliser price has soared by more than 70% this year given the threat to future supply (Chart 2).

Chart 2: Urea fertiliser price has soared due to the threat of future supply

Source: LSEG Datastream. Urea FOB US Gulf futures contract prices.

The ‘double edge’ plough for farmers

The longer the Iran War continues, the greater the upside risks to crop prices such as wheat, corn and rice, which frequently depend on fertiliser. The FAO notes that rising fertiliser costs could impact farmer’s planting decisions “for 2026 and beyond”. The challenge for global farmers is that they confront a ‘double edge sword’ of both rising fertiliser and fuel costs before ploughing. There is the potential that farmers may consider lower plantings to keep their costs manageable. This will only magnify the impact on final retail food prices given a lower supply of crops.

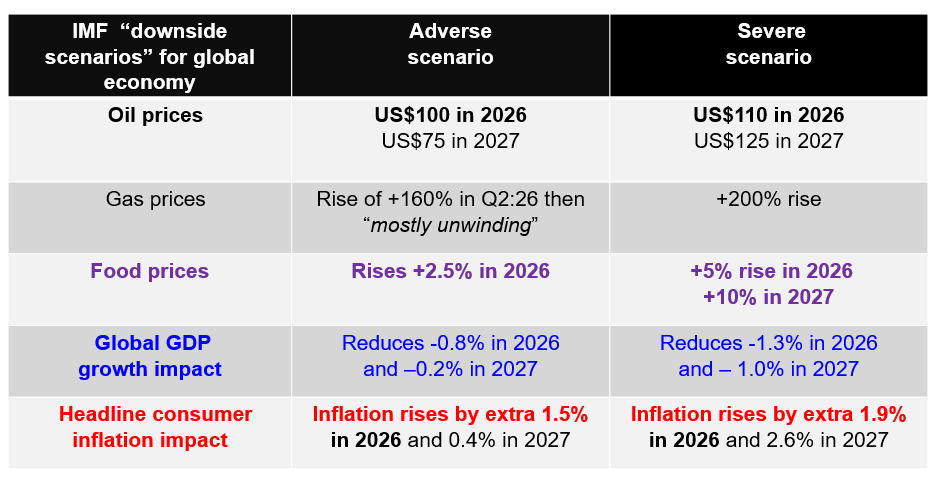

“Tell us the price”

Given the complex dynamics of global commodity prices, inflation, economic activity as well as politics, a forecaster needs to be either brave or reckless in predicting future outcomes. The International Monetary Fund (IMF) has recognised this in their April outlook by considering two different “downside scenarios” (Table 1). The first scenario is called “adverse” and is based on the Iran War ending in 2026. The “severe” scenario contemplates a “larger and more persistent shock” that extends into next year.3

Table 1: International Monetary Fund’s two top-down model-based downside scenarios

The IMF’s “adverse” scenario has a significant impact in reducing global economic growth by -0.8% to 2.3% and by increasing inflation by 1.5% in 2026. The “adverse” scenario sees the impact of the Iran War moderate in 2027 as the shock subsides. Clearly more troubling is the “severe” scenario which dramatically reduces global growth in 2026 and 2027 and raises inflation by circa 2% for both years.

Are we moving from ‘bad to cursed’?

Australian consumers were already troubled by rising consumer prices before this Middle East conflict began. The Federal Government’s recent termination of electricity rebates as well as persistent price pressures in food, health and housing were squeezing household budgets. Australia’s Consumer Price Index for the year to March 2026 showed annual headline inflation was running at 4.6%. There is the prospect of a further interest rate rise in May by the central bank.

For those households with mortgages, their pain threshold was already being tested by rising interest rates in February and March. The extra “cost of living” squeeze from both rising consumer prices and mortgage interest rates is likely to weigh heavily on Australian consumer spending over coming months. Australia’s economy is at risk of suffering stagflation this year with both inflation and unemployment heading higher.

However, this ominous tide of damaging economic consequences could be suddenly reversed if negotiations occur between the warring nations. But this depends on political leaders in the US and Israel realising that their agenda of neutralising Iran’s supposed ‘imminent nuclear threat’ has been achieved and abandoning other objectives such as Iranian ‘regime change.’ This also depends on Iran’s new leadership being willing to talk after the brutal surprise attack. Regrettably, there is still a chasm between the warring parties in terms of trust.

As the IMF warns, there is no predictable path for the Iran War and the global economic impacts:

“The global economic impact will crucially depend on the conflict’s duration, intensity, and scope, which are inherently unpredictable.” 3

1 ‘Oil Market Report - March 2026’, International Energy Agency (IEA), iea.org/reports/oil-market-report-march-2026, published 12 March 2026.

2 ‘Conflict in the Near East region adds pressure on fragile agrifood systems, FAO Director-General warns’, Food and Agriculture Organization of the United Nations (FAO), fao.org/newsroom/detail/conflict-in-the-near-east-region-adds-pressure-on-fragile-agrifood-systems--fao-director-general-warns/en, published 20/04/2026.

3 ‘World Economic Outlook - Global Economy in the Shadow of War’, International Monetary Fund (IMF), Chapter 1. Global Prospects and Policies, imf.org/-/media/files/publications/weo/2026/april/english/text.pdf, April 2026.

Important information

This communication is provided by NULIS Nominees (Australia) Limited (ABN 80 008 515 633, AFSL 236465) as trustee of Plum Super the MLC MasterKey Fundamentals Super and Pension and MLC MasterKey Business Super products which are a part of the MLC Super Fund (ABN 70 732 426 024 (together ‘MLC’ or ‘we’), part of the Insignia group of companies (comprising Insignia Financial Ltd ABN 49 100 103 722 and its related bodies corporate) (‘Insignia Financial Group’). The Insignia Financial Group is ultimately controlled by CC Capital Partners LLC and its affiliates (a New York based private equity firm) and OneIM GP LLC and its affiliates (a London based private equity firm). The capital value, payment of income and performance of any financial product referred to in this communication are not guaranteed. An investment in any financial product referred to in this communication is subject to investment risk, including possible delays in repayment of capital and loss of income and principal invested. No member of the Insignia Financial Group guarantees or otherwise accepts any liability in respect of any financial product referred to in this communication.

The information in this communication may constitute general advice. It has been prepared without taking account of an investor’s objectives, financial situation or needs and because of that an investor should, before acting on the advice, consider the appropriateness of the advice having regard to their personal objectives, financial situation and needs. Investors should obtain the relevant Product Disclosure Statement or other disclosure document relating to any financial product which is issued by MLC, and consider it before making any decision about whether to acquire or continue to hold the product. A copy of the Product Disclosure Statement or other disclosure document is available on mlc.com.au or plum.com.au.

Past performance is not a reliable indicator of future performance. The value of an investment may rise or fall with the changes in the market. The performance returns in this communication are reported before deducting management fees and taxes unless otherwise stated. Actual returns may vary from any target return described in this communication and there is a risk that the investment may achieve lower than expected returns. Any projection or other forward-looking statement (‘Projection’) in this document is provided for information purposes only. No representation is made as to the accuracy or reasonableness of any such Projection or that it will be met. Actual events may vary materially.

This information is directed to and prepared for Australian residents only. Any opinions expressed in this communication constitute our judgement at the time of issue and are subject to change. We believe that the information contained in this communication is correct and that any estimates, opinions, conclusions or recommendations are reasonably held or made as at the time of compilation. However, no warranty is made as to their accuracy or reliability (which may change without notice) or other information contained in this communication.

MLC may use the services of any member of the Insignia Financial Group where it makes good business sense to do so and will benefit customers. Amounts paid for these services are always negotiated on an arm’s length basis.

Bloomberg Finance L.P. and its affiliates (collectively, ‘Bloomberg’) do not approve or endorse any information included in this material and disclaim all liability for any loss or damage of any kind arising out of the use of all or any part of this material. The funds referred to herein is not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds.